Some time ago, another Wingman taught readers how to write a check. I thought I’d go a step further and explain the rules for each component. It’s good to know these guidelines when writing a check, but especially important when trying to cash or deposit a check.

- Date: May not be postdated or stale dated. Postdated is when the date written has not yet happened. Payees must wait until the check’s designated date to present the check for payment. The depositing bank may accept it, but the paying bank could deny it because of the date discrepancy. A stale dated check is one that is more than 6 months old. According to the FDIC, no bank is obligated to accept a stale dated check.

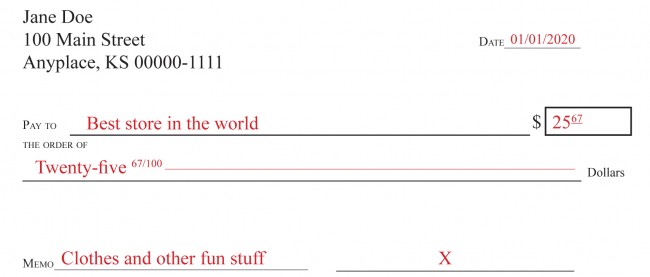

- Payee: The payee, as designated by the check’s remitter, must be the one to endorse the check and take ownership of the funds. The only exception is if the payee signs the check with a special endorsement, making the check payable to another person.

- Legal Line: The legal line is where the remitter designates the check’s dollar amount in written word. You also write the dollar amount in numerical form to the right of the legal line. These two amounts must match! If they do not, the bank will refer to the legal line for payment.

- Signature: The remitter must have signed the front of the check. Without a signature the check is no good.

- Legibility: The check must be legible and the motive clearly stated. Since checks should be written in pen (to prevent alterations), mistakes happen. If writing a check and you make an error, correct it legibly and mark the edit with your initials. Don’t use white out. If it is messy, or you are trying to reuse a check that was originally intended for a different payee, don’t use it! Void it out and write a new check. Banks have the right to refuse any checks that appear altered. Why risk writing or accepting a check that could be turned away?

An additional pointer to leave you with: a valid check will always have a routing number and check number printed along the bottom of the check. This is called the MICR line. If someone hands over a check without a MICR line, you should hand it right back.

Tags: checks, endorsement, legal line, payee, stale date

What if a bank pays a check that has no remitter signature? What can be done, legally?

If a check that you did not sign clears your account, and was not authorized by you, you will want to contact your bank so that they can look into getting the check returned as unauthorized.